Institutional DeFi Pools: The Wall Street Fork of 2026

Executive Summary: The dream of "Unbanked" DeFi lives on, but the money has moved to "Banked" DeFi. Institutional DeFi Pools—permissioned environments requiring KYC/AML—now hold over $200 Billion in TVL. This article explores how Aave Arc, Compound Treasury, and Maple Finance have built a parallel financial system that merges blockchain efficiency with banking compliance.

Introduction

In 2022, "DeFi" meant a teenager in Singapore lending to a hedge fund in New York anonymously. In 2026, that transaction is illegal for the hedge fund.

To capture the trillions of dollars sitting in traditional asset management, DeFi had to evolve. It had to build a fence. Institutional DeFi Pools are identical to protocols like Aave or Uniswap in code, but they add a Whitelisting Layer on top. You cannot interact with the smart contract unless your wallet address has a "Soulbound Token" proving you have passed KYC/AML checks.

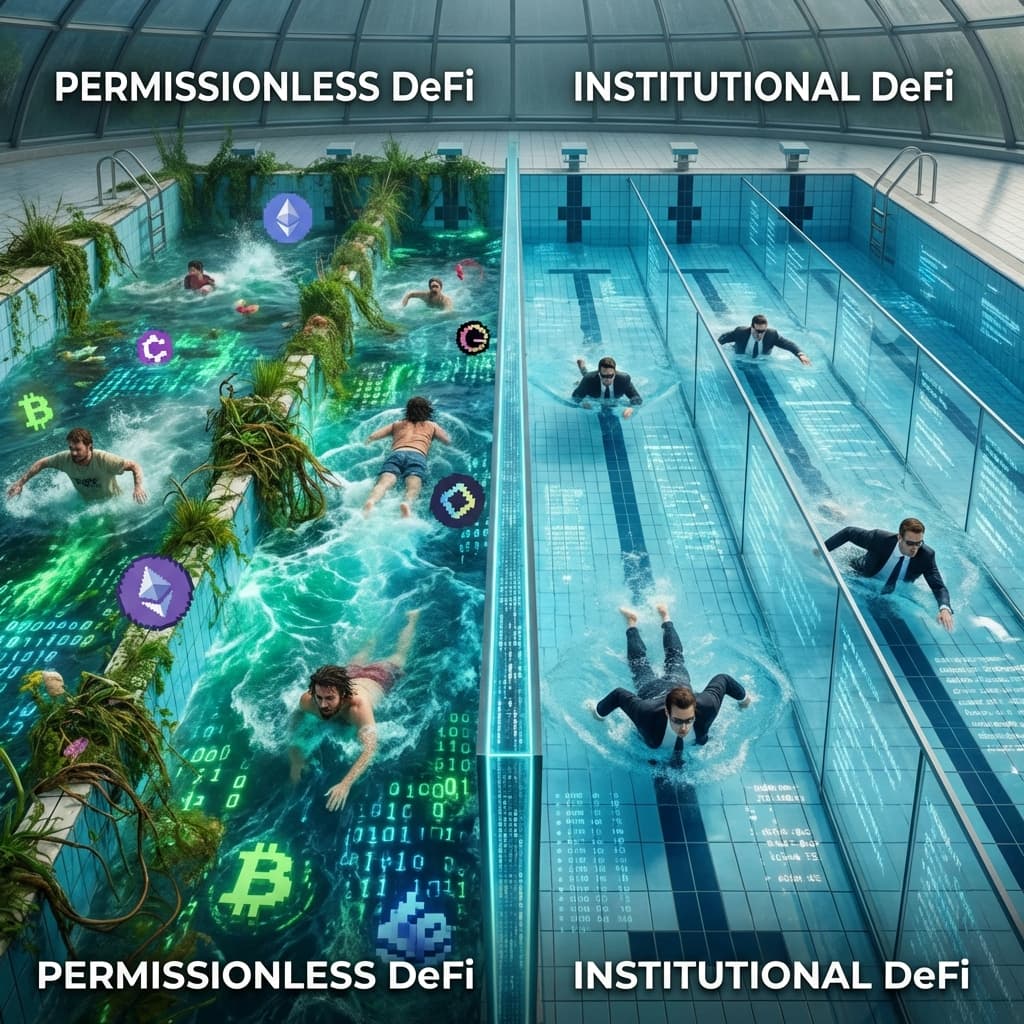

The "Walled Garden" Ecosystem

This parallel system allows giants like BlackRock, JP Morgan, and Siemens to trade and lend to each other without fear of interacting with sanctioned wallets or money launderers.

Key Platforms of 2026

- Aave Arc: The leader. Institutions lend USDC to each other. The rates are lower than "Retail Aave" (swimming with the sharks), but higher than traditional T-Bills. It operates as a 24/7 repo market for the banking sector.

- Compound Treasury: Now fully integrated with Neobanks. It offers a fixed 4% APR to corporate treasuries, handling all the crypto complexity on the backend.

- Maple Finance: The credit market. Specialized "Pool Delegates" (credit analysts) underwrite loans to crypto-native market makers. In 2026, Maple defaults are enforceable in Delaware courts, making it a true hybrid of DeFi and TradFi law.

Why Institutions Bother with DeFi?

If they have to do KYC anyway, why not just use a bank? Efficiency.

- T+0 Settlement: A trade on Wall Street takes 2 days to settle. On Aave Arc, it settles in 12 seconds.

- Programmability: A fund can write a smart contract to "Sweep cash into Aave Arc every Friday at 5 PM and withdraw it Monday at 8 AM." This automation of idle capital catches interest that used to sleep over the weekend.

- Transparency: Auditors can verify the fund's solvency on-chain in real-time, removing the need for quarterly "Proof of Funds" PDF reports.

The "Liquidity Fracture"

This has created a controversial Liquidity Fracture.

- Public Pool: High risk, high yield, retail + degens.

- Permissioned Pool: Low risk, lower yield, institutions.

Arbitrage bots bridge the gap. If rates on Public Aave go to 10% and Permissioned Aave is 4%, whitelisted bots (who have access to both) borrow cheap from institutions and lend to retail, closing the spread while pocketing the difference.

FAQ

Q: Can I join Aave Arc? A: Not unless you are an institution. You need to go through a "Whitelister" (like Fireblocks) and prove you are a compliant corporate entity.

Q: Is "Permissioned DeFi" an oxymoron? A: Purists say yes. It's not "Decentralized" if there is a gatekeeper. But pragmatists say it's the only way to onboard the world's GDP. It uses decentralized rails (Ethereum) but centralized access.

Q: What is a Soulbound Token (SBT) in this context? A: It's an NFT that cannot be transferred. It sits in your wallet and says "This wallet belongs to a verified US Corporation." The Aave Arc contract checks for this token before letting you deposit.

Q: Does Uniswap have a pro version? A: Yes, Uniswap KYC Hooks. In v4, liquidity providers can choose to create pools that only accept KYC'd traders. This is popular for trading regulated Security Tokens.

Q: Will the two worlds ever merge? A: Likely not. Regulatory "Travel Rules" require identifying counterparties. We will likely see two permanent parallel streams: the "Wild West" (Retail) and the "Walled Garden" (Institutional), connected only by arbitrageurs.

Conclusion

Institutional DeFi is the bridge between the sterile world of banking and the chaotic innovation of crypto. In 2026, it is no longer a science project; it is the plumbing for next-generation capital markets. Code is law, but KYC is the key.

Related Articles

Stablecoins: The New Global Settlement Rails

SWIFT is too slow. Visa is too expensive. In 2026, Stablecoins settle $50 Trillion annually, becoming the default layer for cross-border B2B payments.

BNPL 2.0: The B2B Credit Revolution

Buy Now Pay Later isn't just for sneakers anymore. In 2026, B2B BNPL allows companies to finance cloud costs, inventory, and SaaS subscriptions on-chain.

Tokenized Mortgages 2026: Home Ownership on the Blockchain

The 30-day closing period is history. Tokenized mortgages allow for instant settlement, fractional ownership, and global liquidity for real estate debt.